One of the most essential tools in restaurant accounting to effectively manage food cost is a Declining Budget. When used properly, a Declining Budget can be one of the best tools for stabilizing your costs as well as increasing your cash flow.

What is a Declining Budget?

A Declining Budget is used in the restaurant industry to help controllers and operators manage operational costs – more specifically, the relationship between sales (revenue) and the amount spent in relation to those sales. Ultimately a Declining Budget will support management in monitoring variable spending and fluctuating sales (revenue).

The two parts of a Declining Budget:

To grasp how we use a Declining Budget, we must first identify the two vital factors for its success: restaurant Sales (Revenue) and Product Pricing.

#1) Restaurant Sales (Revenue)

Factually, restaurant revenues are variable. Many restaurants obtain revenue from multiple revenue centers, with Dining Room, Bar, Catering, Banquets, and Retail as the most common.

Each week, the sales from these revenue centers can vary widely based upon seasonality, weather, holidays, sporting events, construction, and new competition.

#2) Product Pricing

Product pricing also fluctuates tremendously based upon seasonality, availability, purchase quantity, quality, and total purchases made with a specific vendor.

Added to the instability is that products have varying shelf lives (the length of time a product can remain on the shelf before it spoils). Shelf lives can range from one day for produce to indefinite for items such as paper supplies.

It’s easy to budget how much you’re going to spend (and ultimately make) when both the revenue you bring in and the product costs are static, but that’s simply not the nature of the game.

Examples of a Declining Budget: What NOT to do vs What TO do!

Our sales can easily decline for the last four weeks because of the weather, a big sports game, or the holiday season.

Example #1) What NOT to do:

- Monthly Sales Revenue:

- WK 1 Sales: $20,000

- WK 2 Sales: $17,000

- WK 3 Sales: $15,000

- WK 4 Sales: $14,500

Looking at the sales above, we’re $13,500 off in revenue from the 1st week through the 4th week ($20,000 – $14,500 = $13,500).

So, what happens if we spend the same amount of money buying our product each week, without actually knowing that we should reduce it based on the sales?

- Monthly Product Costs:

- WK 1 Costs: $10,000

- WK 2 Costs: $10,000

- WK 3 Costs: $10,000

- WK 4 Costs: $10,000

Total Product Costs = $40,000

- Monthly Cash Position:

- WK 1 Cash: $20,000 sales – $10,000 product cost = $10,000

- WK 2 Cash: $17,000 sales – $10,000 product cost = $7,000

- WK 3 Cash: $15,000 sales – $10,000 product cost = $5,000

- WK 4 Cash: $14,500 sales – $10,000 product cost = $4,500

Total Cash On Hand = $26,500

Total Cash On Hand $26,500 – Total Product Costs $40,000 = $13,500 of OVERSPENDING in one month.

Ultimately, using a Declining Budget gives you the ability to keep one eye on the fluctuation in your sales, and the other on how much you’ve spent IN RELATIONSHIP TO THOSE SALES. Thus, if used daily, supports keeping your variable spending in line with your fluctuating sales.

WATCH THE FULL VIDEO BELOW!

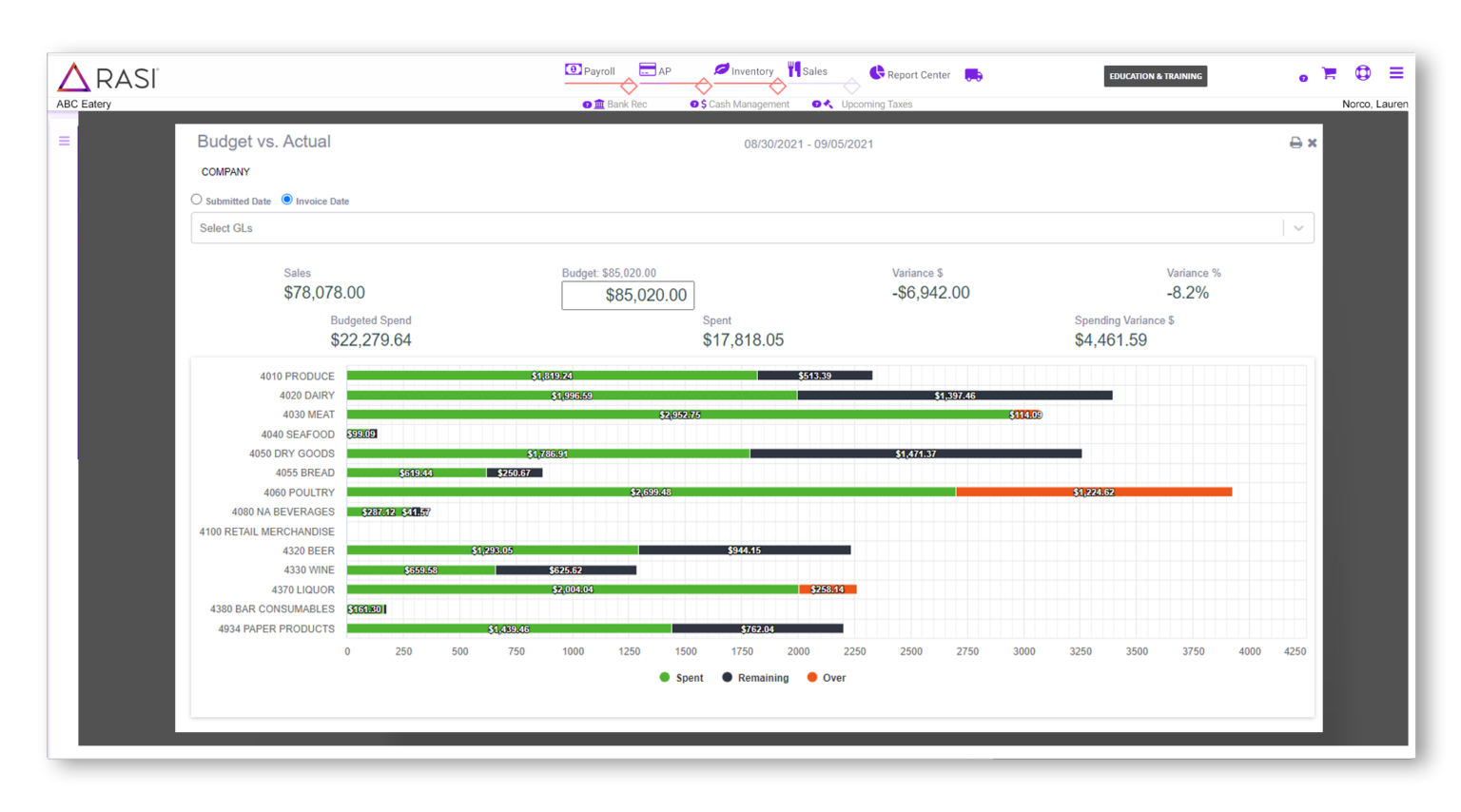

Example #2) What TO do! A Declining Budget

In the example above, we’re stating the following:

- Total budgeted revenue = $85,020.00 for the week

- Total budgeted spend = $22,279.64 for the week

- Current revenue = $78,078.00 for the week

- This means we’re off in revenue by $6,942 or 8.2% for the week ($85,020.00 – $78,078.00 = $6,942.00)

- Total spend on Cost of Goods and Paper Products = $17,818.05 for the week

- This leaves $4,461.59 before exceeding the budgeted spend for the week ($22,279.64 – $17,818.05 = $4,461.59)

- Digging deeper into your costs, looking at Produce, you have $513.39 remaining before you exceed your budget, whereas Meat has already exceeded your budget by $114.09.

How a Declining Budget actually works:

Each day, your sales are updated, and your purchases are recorded. The total purchases are summarized and subtracted against the forecast. The result is your available spend amount.

What happens when you spend more than your budget amount?

You shouldn’t spend over your limit. However, when you do, it typically means one of a few things:

- Is your revenue forecast accurate? Pay attention to your daily sales and make adjustments. Not doing so places your operation in a bind. For example, if you notice that your week is busier than usual, but you don’t adjust your spending accordingly, you may not order enough product to satisfy all of your hungry guests.

- Are your targets reasonable? Can you run a 33% food cost when you’ve been averaging 38%? It is vital to be realistic in your expectations. Targeting too low won’t allow you to spend enough on product to service your forecasted sales (even when they are accurate).

- Do you have the “Gallon of Gas Syndrome”? You’ve forecasted your revenue correctly, and you’re ordering the correct amount of product. However, you’re still overspending. The Gallon of Gas Syndrome simply means you can only go so far with what you have. Product prices are volatile, especially on produce, dairy, meat, and seafood. They change weekly. Thus, staying disciplined and following a Declining Budget enables you to notice pricing fluctuations on critical items. In turn, this allows you to work with your vendors proactively on procuring the highest quality products while sticking to your budget.

Note: A good rule of thumb is to forecast on Monday and make your adjustments on Thursday (prior to placing your weekend orders).

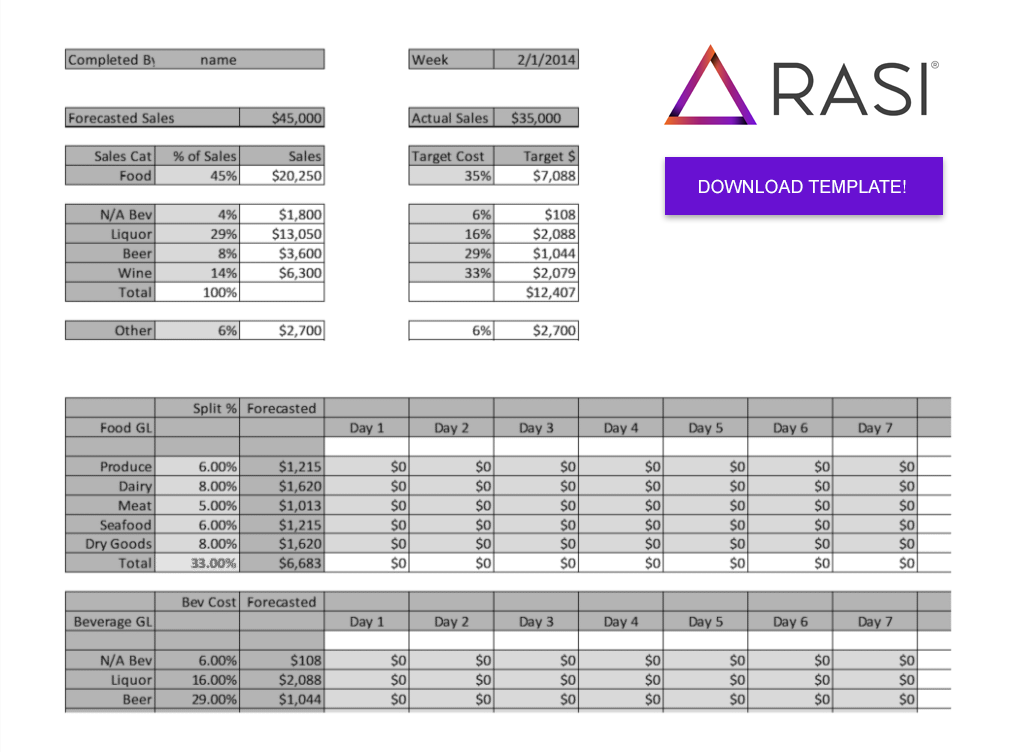

Get the basic Declining Budget template below!

Download a basic version of a restaurant Declining Budget below. It will get you started and give you a sense of what you need to start taking charge of your finances.

LISTEN TO THE FULL PODCAST EPISODE BELOW!