Every restaurant operator should review the Cash Flow Statement on a regular basis. It can be an incredibly valuable tool for your business if used properly. Restaurant owners and operators have become accustomed to reviewing the Balance Sheet and P&L, but in the grid of focusing on all the aspects of the restaurant that need attention, the Cash Flow Statement often gets lost in the mix.

Every restaurant operator should review the Cash Flow Statement on a regular basis. It can be an incredibly valuable tool for your business if used properly. Restaurant owners and operators have become accustomed to reviewing the Balance Sheet and P&L, but in the grid of focusing on all the aspects of the restaurant that need attention, the Cash Flow Statement often gets lost in the mix.

Flattening The Cash Flow Curve:

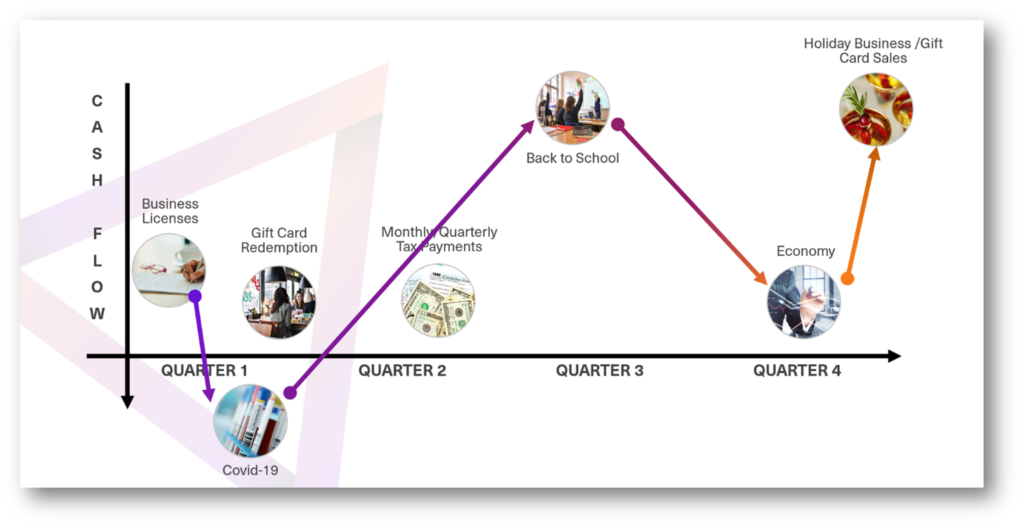

Restaurants are in a uniquely difficult situation when compared to other business segments. Many cash flow impacting events make managing a bank account (most importantly keeping a bank account positive) extraordinarily difficult throughout the year.

Firstly, there are natural sales affecting trends that significantly affect your guest traffic-holiday sales, weather, back to school, and patio sales, to name a few. Additionally, gift card sales have a hugely positive impact when you sell them but negatively impact cash when redeemed. As restaurant owners and operators have recently learned, a pandemic with government restrictions can test even the most successful operations.

Being strategic with cash-impacting events that you have the most control over will help flatten the curve and mitigate the impact of unexpected cash-affecting events. A good finance manager is going to be strategic about the cash impacting events they have the most control over; examples include:

• When am I paying off my loan?

• When am I dipping into my LOC?

• When will that tax credit hit?

• When should I invest more in my business, and when should I purchase capital expenditures?

If you can strategically plan around cash-impacting events, you will be able to flatten the curve and the EKG chart of your bank balance (as seen above). This may seem obvious, but too many restaurants learn this the hard way and are forced to react to low bank account balances instead of being proactive. When rash, you are more likely to make poor business decisions, like going for predatory high-interest rate loans that get you the cash quickly. Proper planning will help to prevent this!

Forecasting & Budgeting

To successfully create a precise budget or properly forecast sales, you must be knowledgeable about your breakeven points when it comes to sales. These points may be significantly different now than they were two years ago, so keeping up to date on your breakeven numbers is always a best practice. A breakeven factors in your variable and fixed costs and showcases what you need to recoup in sales to break even.

There are two kinds of break evens a restaurant should be reviewing:

- A cash flow breakeven: A cash flow breakeven not only factors in your restaurant profitability but also your debt servicing, government assistance, and anything else that does not show up on your P&L but needs to be factored into your cash management strategy.

- An operational breakeven: The breakeven from an operational standpoint is determining the following: “Can my restaurant OPERATIONALLY stand on its own two feet?” This is an important activity for any restaurant and helps you determine budgets, goals, and operational directives.

A budget allows you to set goals for your team and plan expectations for costs and revenue despite small adjustments within a period. This can be tracked on a week-by-week and period-to-period basis to determine how well you’re performing in compared to your goals.

For example, If it snows and you don’t hit your target for a specific week, that’s when you would utilize a forecast to ensure proper spending based on actual sales. However, your overall budget for the year wouldn’t change, so you would still aim to hit your budgeted cost. Forecasting and adjusting based on actual sales allows you to hit your budget goals continuously.

WATCH THE FULL VIDEO BELOW!

The Balance Sheet

The Balance Sheet is one of the most important financial statements as it shows the business’s true worth. If the Balance Sheet is inaccurate, the chances are that your P&L and Cash Flow statement are inaccurate as well, and more times than not, the result is not in your favor as expenses are missing. Inaccuracies could lead to cash flow problems, so consistently verifying the balances on key accounts is critical to your business.

Reviewing Current Assets:

- When reviewing current assets, verify that your House Bank reflects your restaurant’s true balance of cash. If not monitored, House Bank can be a catch-all for random transactions. Keeping an eye on this balance keeps your operators honest and prevents theft.

- If you have outstanding House Accounts or Accounts Receivable, it’s best to immediately collect that payment to increase cash flow and verify outstanding balances.

Reviewing Liabilities:

- When reviewing liabilities, you should always keep your eyes on your Credit Card Tips account. This account should never hold a balance if you are doing weekly payroll. Keeping this account clear avoids audit discrepancies and hours of research.

- Gift Cards payable will show you the value waiting to be redeemed. Planning for this, primarily through the holidays, is critical for cash flow. This is money you have already received, but there won’t be any cash coming in when the product goes out.

- Finally, verify that the credit card balances reflected match your most current Credit Card Statements. If you find a negative balance reflected on a credit card payable, that could mean you have expenses that haven’t been appropriately reflected on your P&L.

Reviewing Inventory Levels:

Another great tactic for increasing cash flow is reviewing your current inventory levels. Managing inventory is a balance between ensuring you have what you need to take care of your guests and your team and not inflating inventory on the shelves, which negatively impacts cash flow. If you’ve never performed inventory, make sure you’re utilizing a declining spending budget week-over-week based on your new anticipated sales, so you are not over-purchasing.

Financial Statement Review:

Owners and operators should be reviewing cash flow each period. A Financial Statement Review goes through each line of your balance sheet to confirm the balance. Conducting these types of reviews enables the isolation and cleanup of any inaccuracies, allowing you to gain a true understanding of what is living on your balance sheet while actually understanding those current balances. Additionally, financial statement reviews showcase training opportunities for your team and why certain adjustments may have been made.

Period End Financial Close:

The Period End Financial Close focuses on five steps to properly close the period:

- Running your business

- Grading your performance

- Conducting the financial review

- Theft prevention and accuracy

- Reviewing the cash flow statement

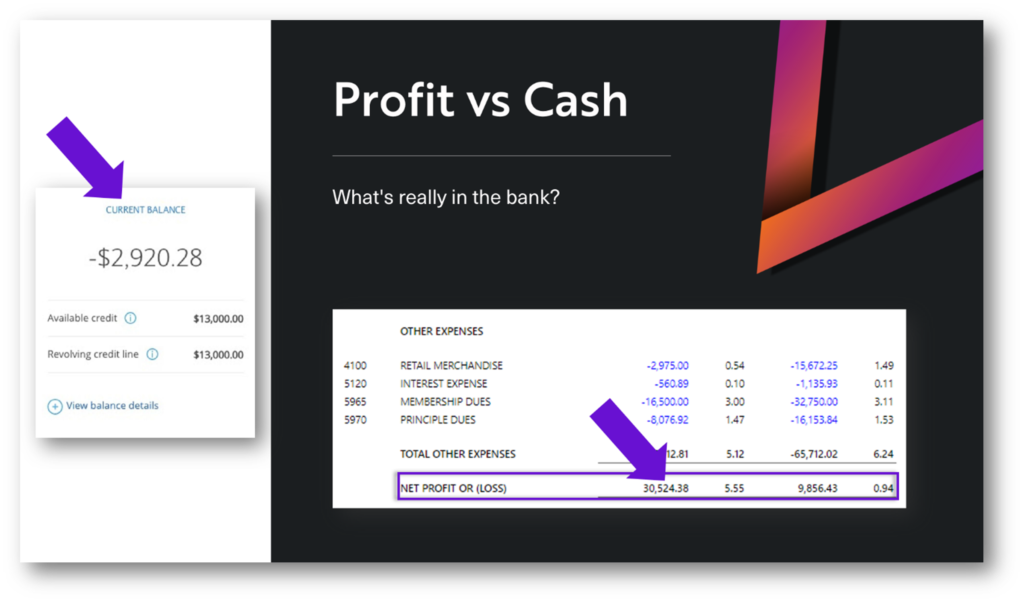

A complete Period End Financial Close keeps eyes on your financial statements and helps in ensuring accuracy period over period. Once you have confirmed that your Balance Sheet is accurate, you can trust that the Net Profit on your P&L is accurate; however, profit doesn’t necessarily equal cash in hand.

The profit from your P&L is only one small part of the items that have an impact on your cash flow. Any changes to your balance sheet (assets, liability, etc.) also have an impact on your cash flow. For example, if you pay off a $100k loan, this does not show up on your P&L. This reduces liability on your balance sheet and has a negative impact on your cash balance (great, healthy business activity, but negative impact on cash).

Understanding The Cash Flow Statement

Common cash flow statement misconceptions:

- The cash flow statement represents your bank balance: The cash flow statement takes into consideration all cash activity within a specific time frame, but those transactions potentially haven’t cleared the bank. All deposits and outstanding checks and transactions would have to clear in one day for it to reflect your bank balance.

- A reduction of cash reflected on the cash flow statement is a negative concept: While a reduction on the cash flow statement does mean a decrease in cash flow, that is not always a bad thing. As mentioned above, if you pay down a credit card or loan, you are increasing the worth of your business by paying off debt, which is a positive activity for your business.

- Strong profits result in healthy cash flow: The cash flow statement is a combination of your P&L and Balance Sheet; just because you show a profit on the P&L doesn’t mean that cash flow is strong; there could be liabilities on the Balance Sheet that are reducing that cash flow.

- Reviewing the P&L and Balance Sheet is enough: The cash flow statement is the best way to view your true cash position and overall financial health.

- As a small business owner, I don’t need a cash flow statement: Regardless of size, any business must have eyes on the cash flow statement.