Experienced restaurant operators closely manage the inflows and outflows of cash through their business. Sound management of available cash is critical to the ability to pay wages, keep the lights on, stock the walk-in, and make distributions to owners.

The financial document that summarizes these transactions is known as the restaurant cash flow statement. An understanding of this document is important not just for your accountant, but for owners and managers as well. Once you can interpret your cash flow statement, you’re in a position to more accurately project the future financial health of the restaurant.

What is a Cash Flow Statement?

The restaurant cash flow statement records incoming and outgoing cash over a defined period of time, typically a quarter or fiscal year.

Simply put, your restaurant cash flow is profits made minus all operating costs. Profit is all the cash remaining after all expenses are paid, while restaurant cash flow is the flow of money into (sales, accounts receivable, etc.) and out of (expenses, operating costs, etc.) the restaurant.

It also represents how the Balance Sheet and P & L work together to impact your cash and operating accounts.

Because restaurants don’t operate entirely on a cash basis, it’s often difficult to find your cash position from the Income and Expense Statement and the Balance Sheet alone.

Incoming cash includes revenue earned from sales of food and beverages, merchandise, rental income, as well as less common sources such as income from loans, financial assets, and investments from owners and partners.

Outgoing cash records payments made for wages and salaries, operating expenses such as utilities and laundry service, and financial expenses, such as payments of dividends.

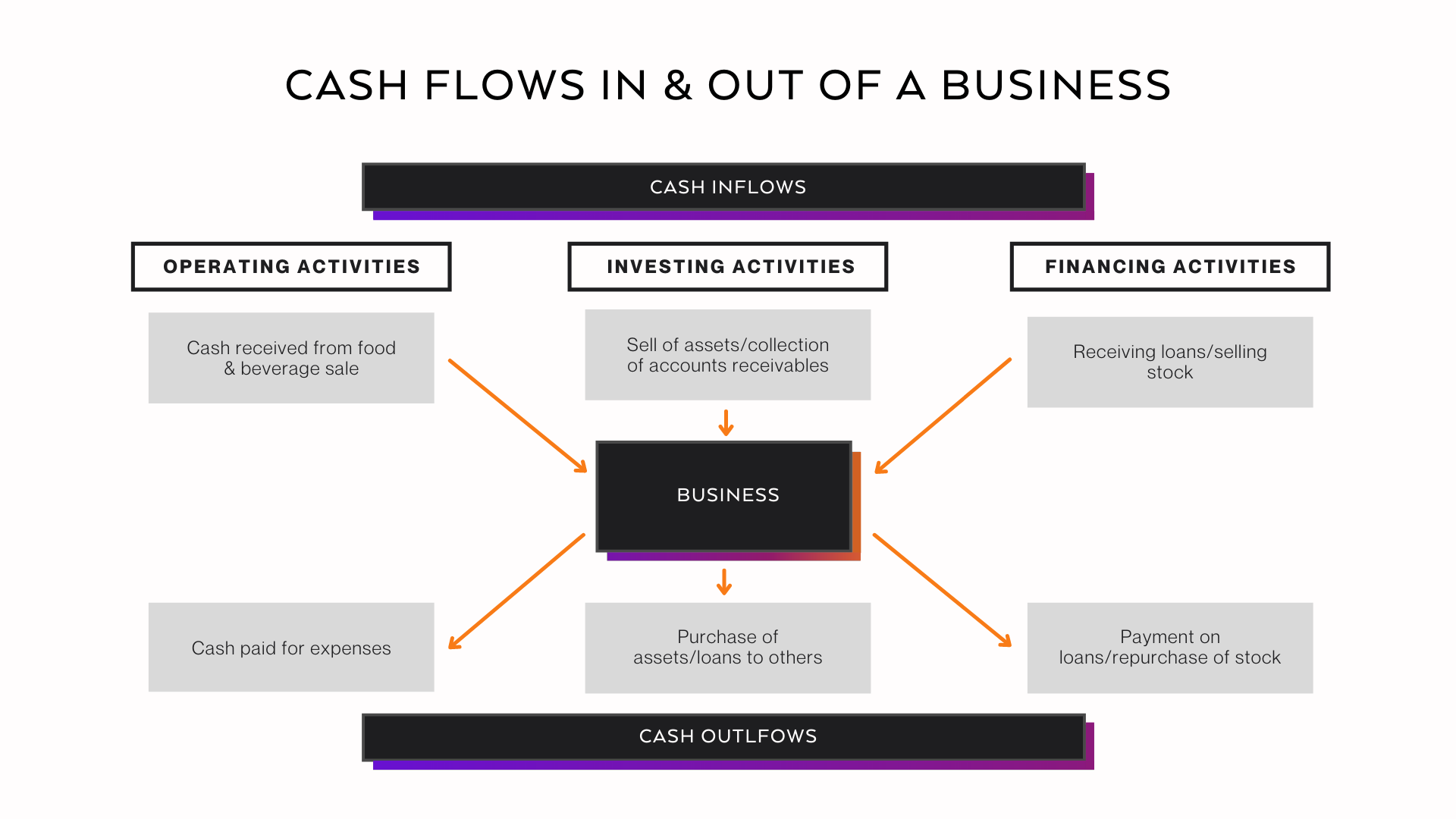

By accounting convention, the cash flow statement is divided into three parts, cash flow operating activities, investing activities, and financing activities.

What does a Cash Flow Statement Show?

How can Restaurant Operators use the Cash Flow Statement? Operators can utilize the cash flow statement both internally and externally.

For internal purposes, operators should review the statement every period to understand where cash is going and where it is coming from. A few questions to ask include:

- Were there any large purchases or loans taken out on the business?

- Was the operational cash provided enough to cover the large asset purchase or payment on the note?

For external uses, banks use the cash flow statement to decide on the creditworthiness of the business.

They may be looking to learn items like does the restaurant make enough cash to cover its current liabilities through the operations? Or, where exactly is the cash coming from?

The Relationships Between Your Restaurant Financial Statements

Restaurant Cash Flow Statement:

Displays the cash activities from both the balance sheet and the Income & Expense Statement.

It represents a combination of activities resulting from the daily operations illustrated on the Income & Expense Statement (P&L) and the business’s overall activities and “health” as represented on the Balance Sheet.

A restaurant cash flow statement demonstrates the effect that cash inflows and cash outflows have on the business’s cash position. (We’ll dive deeper into the breakdown of the cash flow statement throughout the article).

Income & Expense Statement or Profit and Loss Statement (P & L):

Reports on the business’s day-to-day operations for a set time frame.

The P&L begins with all revenue from your sales within the restaurant. Not all sales provide cash to the bank on the same day of the sale – for example, A/R and Third-Party Delivery Services.

It then subtracts operational expenses – from labor, food purchases, and direct operating, administrative expenses, and occupancy costs.

While expenses may be recorded in real-time as you pay your vendors, the vendor may not cash that check for several weeks – so while the expense is accounted for, the money is still in your bank.

The amount left after the revenue and the expenses are recorded is your net profit and loss for the business within that time frame

Restaurant Balance Sheet:

The Balance Sheet represents the financial health of the business.

It begins with your assets, or what you own; Items such as your house bank, cash operating accounts, and large asset purchases such as furniture, equipment, and leasehold improvements.

From there, your Balance Sheet goes to liabilities, or what you owe; Items like your accounts payable, tax accounts, credit cards, and long-term debt.

Lastly, the Balance Sheet will show any dividends, retained earnings, as well as your Net Income and Loss.

While the P&L and Balance Sheet are critical to understanding your financial health, they in themselves do not show the true impacts of cash.

How do cash inflows and outflows affect your business?

WATCH THE FULL VIDEO BELOW:

How to read a Cash Flow Statement?

Let’s begin by first breaking down the Cash Flow Statement into all of its smaller parts…

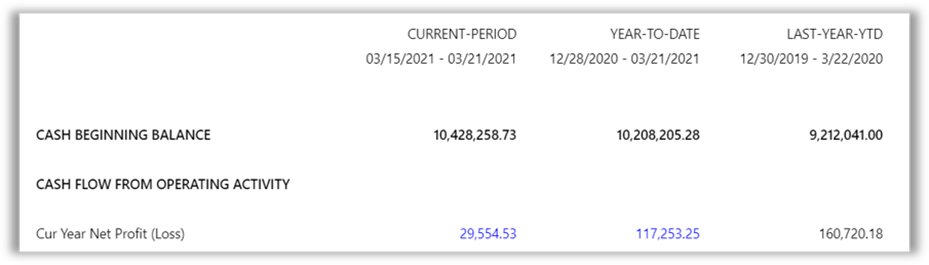

Cash Beginning Balance

The Cash Beginning Balance represents the total balance of all readily available cash accounts from the previous weeks’ balance sheet.

Cash Flow Operating Activities

Cash flow from Operating Activities lists the transactions that form your average restaurant’s bulk of cash flows. Operating activities include the revenue generated from food and beverage sales, merchandise sales, and rental receipts.

Additionally, it records wages and salaries, purchases of inventory, all the miscellaneous expenses of keeping the lights on and the doors open, and changes in accounts receivable and accounts payable.

Net Profit or Loss

The Net Profit/Loss shown on the Cash Flow Statement isn’t what is reflected in your bank account. In the snippet example below, expenses exceeded revenue for the period, however, YTD, there is still a profit.

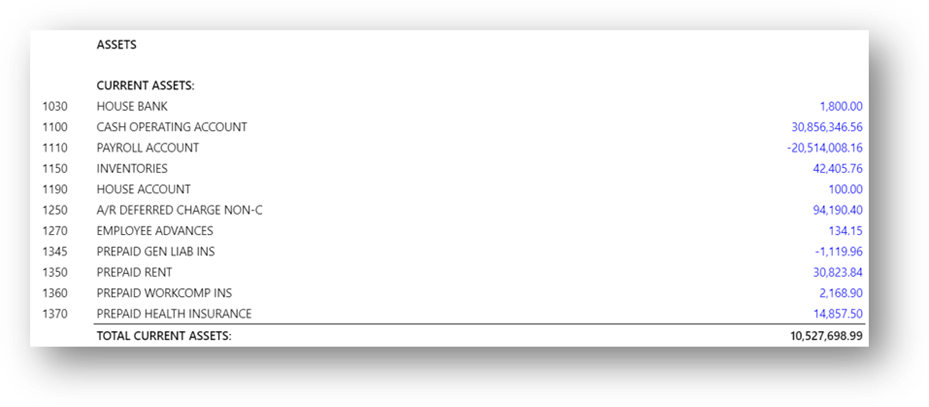

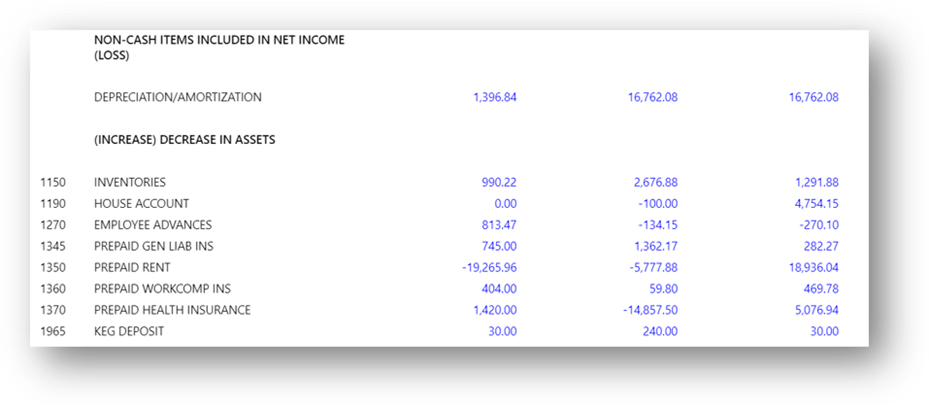

Assets

Assets are what you own. There is a related decrease in cash flow when there are increases in assets.

Example: Inventory on the shelf is money that is not in the bank – An increase in the inventory asset is a decrease in the cash in the bank.

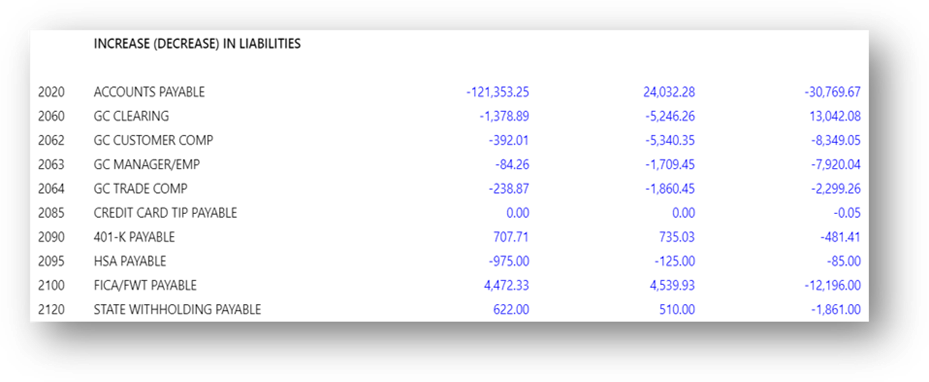

Liabilities

Liabilities are what you owe. When there is an increase in liabilities, there is also an increase in cash flow.

Example: Gift Cards are an increase to cash when they are sold, but a decrease to cash when they are redeemed – this is important to consider when forecasting cash flow during slow months.

Investor Activity

Cash marked under Investing Activities covers changes in assets, such as the purchase or sale of land, the purchase or sale of equipment, loans to vendors, and changes in holdings of stocks and securities.

In your average restaurant, you’re most likely to see cash-out transactions for expenses like kitchen stoves and refrigerators in this section of the cash flow statement.

When there are increases in investor activities, there are decreases in cash flow.

Example: Leasehold improvements will decrease cash to pay for the improvements – Forecast preventative maintenance schedules and large expenses when forecasting out cash flow for these expenses.

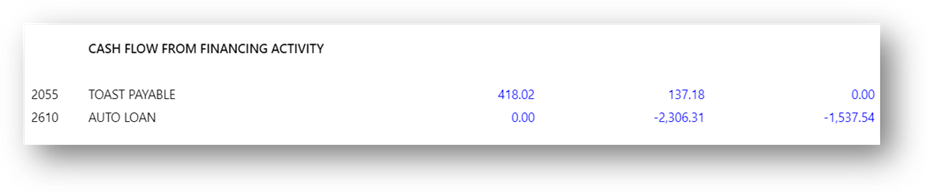

Financing Activity

Investments from partners and owners, as well as payments of dividends, constitute Financing Activities. This is where direct investments of cash into the business show up, as well as withdrawals/distributions to owners. When there is an increase in financing activity, there is also an increase in cash flow.

Example: A loan brings money into the business, increasing cash and increasing liability – Consideration should be taken into the payment of the loan vs. available cash flow, especially if the loan has a variable payback schedule (mob loans & advances)

Ending Cash Balance – How Are These Numbers Generated?

An increase or decrease in cash represents the total increase/decrease of cash resulting directly from Operating, Investing, and Financing Activities. The ending cash balance, however, showcases the total readily available cash from the current Balance Sheet.

How to calculate Cash Flow Statement?

There are two approaches to the calculation of the cash flow statement, indirect and direct.

Statement of Cash Flows Direct Method

The direct calculation can be as simple as the summing up of all the positive and negative cash transactions in each of the three sections of the cash flow statement, as described above. It can also be measured by the changes in your asset and liability accounts. This cash flow method is used by businesses that are run on a cash accounting basis.

Statement of Cash Flows Indirect Method

Whereas the indirect method statement of cash flows calculation involves making additions and subtractions to the income statement based on cash and non-cash transactions to arrive at your cash flow statement.

For the non-cash transactions, your accountant will consult your balance sheet, recording changes in assets and liabilities. Note that accounts receivable (AR) decreases are added to net earnings, while AR increases are deduced. This method is used by companies that run their accounting on an accrual basis.

Restaurant Cash Inflow & Outflow Example

Let’s look at a cash inflow & outflow example to fully grasp your restaurant cash flow statement. Start with all money coming into your restaurant – this includes regular menu sales, merchandise income, income from catering, promos, and all other money you’re owed.

Now, calculate all outgoing cash; loan payments, rent, utilities, payroll & taxes, inventory expenses, supplies, regular payments, and more.

When figuring out cash outflow for your restaurant cashflow, don’t forget atypical expenses like capital expenditures, overtime payroll, and similar costs.

If your cash inflow equals $85,000 for a fixed accounting period (weekly, bi-weekly, monthly, etc.), and your outflow is $55,000 for the same period, your restaurant cash flow statement will show $30,000.

RASI recommends the smallest possible reporting window of one week for all financial reporting, including for your restaurant cash flow management. This helps ensure you always have the most accurate picture of your restaurant’s finances.

How does software help calculate your restaurant cash flow statement?

The foundation of restaurant cashflow analysis is accurate data on your cash inflows and outflows. For restaurants, that mostly means food and beverage sales (inflows) and wages and operating expenses (outflows). To a large extent, this is data that lives in your POS solution.

To make quick work of your cash flow statement, you want restaurant accounting software that integrates with your POS and pulls out the data for easy categorization and review. RASI’s software is notable for excelling at this function.

Beyond POS data, a cash flow statement requires tracking your accounts receivable (AR) and accounts payable (AP). Ideally, this information should reside inside the same software suite you use to analyze POS data. An integrated restaurant accounting solution puts your AR and AP transactions alongside income, to give you a comprehensive overview of your accounts.

The next puzzle piece in the financial picture of your business is payroll. Recording the wages and salaries you pay is a large part of the cash outflows that fall in the operating activities section of the cash flow statement. A properly comprehensive restaurant accounting solution, like RASI’s, will manage your payroll as well.

How does your cash flow statement help with restaurant profit?

As we’ve shown throughout this article, the cash flow statement for a restaurant is a concise summation of the use of cash by your operation. It records whether your cash inflows are larger than your outflows (key for profitability) and shows you what funds are available for investment in the business, such as equipment purchases.

The cash flow statement is also very useful as a gauge of whether you’re generating enough cash to undertake expansion, as banks will want to see healthy cash flow from your main restaurant before approving loans for additional locations.

Your cash flow statement is a regular measure, in conjunction with the income statement and balance sheet, of the evolving quality of your finances. As a group, these financial statements enable operators to make fully informed operational changes that drive profitability in the business.

How to choose software to keep on top of your cash flow statement

To easily calculate your cash flow statement, you need a complete solution for restaurant accounting. RASI’s comprehensive software integrates POS data, inventory, accounting, payroll, cash management, and operational metrics, eliminating manual data entry and giving you a single point of access for all your restaurant data.

LISTEN TO THE FULL PODCAST EPISODE BELOW!!

RASI is the choice of thousands of restaurant operators across the country. When you sign up with RASI, a dedicated account team will onboard your management staff, configure the software to match your operational flows, and coach your team on how to use the software to set and meet financial goals. Contact us today for a free demo!